2017 MCM Market Horse Race

Feb. 20, 2017 - May 26, 2017

COMPETITION

The competition will be creating a

portfolio through May 26, 2017 using data from Non-US (XUS), Global (GL), and

Emerging Markets (EM) from 1999 - Nov. 2016 for the annual MCM Horse Race!

The(IBM) jrd -guerard file contained updated U.S. information from the original

JOI_GUERARD and Saxena JOI studies of 2011-2012. The underlying, original paper

is entitled “Investing with Momentum” , was published in The Journal of

Investing (JOI-GUERARD). The Global expected returns, run over similar

conditions was published in the IBM Journal of Research and Development, as

06601697.pdf.

The Horse Race conditions are as Follows:

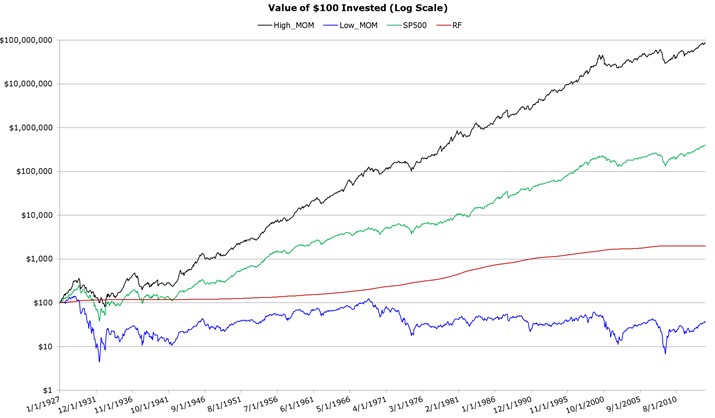

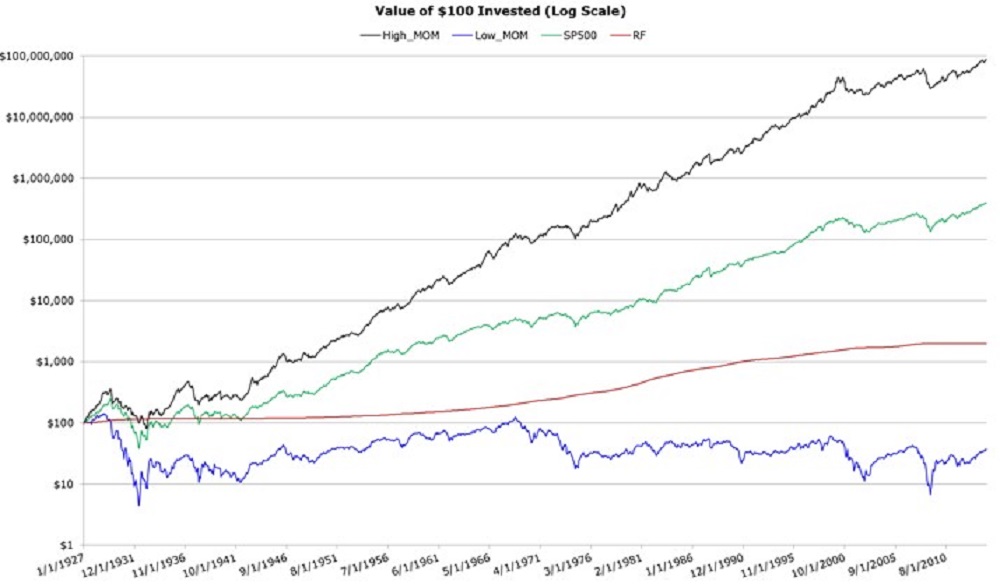

1. Maximize the Geometric Mean over the 1/1997- 12/2016 period using the CTEF

and REG10 (USER, GLER) series (high values are preferred) as tilts;

2. Maximum buy turnover is 8% monthly;

3. Minimum Threshold Position is .35% (35 basis points);

4. Maximum Mean-Variance weight in any security is 4%; one can use benchmark

weight +/- 2%;

Competition Information

Risk-Based and Factor Investing

(Warning Large File Size)

Horse Race of Risk-Based Portfolio Construction Techniques

Efficient Global Portfolios: Big data and investment universes

Feature Selection for Portfolio Optimization

Geometric Mean Maximization: Expected, Observed, and Simulated Performance

International Journal of Forecasting

The Journal of Investing

Improving the Investment Process with a Custom Risk Model: A Case Study with the GLER Model

Global Stock Selection Modeling and Erricient Portfolio Construction and Management

Investing with Momentum: The Past, Present, and Future

The role of effective corporate decisions in the creation of efficient portfolios

Topics in Applied Investment Management: From a Bayesian Viewpoint

An Empirical Case Study of Factor Alignment Problems Using the USER Model

SIGN UP

Click Here to enter the competition and download MATLAB datasets.

Competition complete

CONTACT

For any information regarding the

competition, please email

Dr. Zari Rachev.

SPONSORS

The event is sponsored by the Mathematics and Statistics Department of Texas Tech University and McKinley Capital Management, LLC.